The SaaS Trends Report

Introduction

Over the past 18 months, the software market has undergone a significant transformation.

We have entered a new reality characterized by tighter budgets, more challenging capital markets, and slower growth. These factors have had a substantial impact on the purchasing behaviors of buyers and the sales strategies of sellers.

In Q2 2023, Vendr processed over 3,000 transactions, totaling over $240 million in SaaS spend. This report provides a detailed breakdown, including information on popular categories, average discounts, and our inaugural AI index. Based on our observations from Q2, two prominent trends have emerged:

- Software buyers are actively consolidating their tech stacks, prioritizing existing suppliers and reducing spending on new products.

- Software sellers are increasingly focused on price transparency, evidenced by a gradual decline in average discounts. The discount rate decreased from 11% in 2022 to 9% in Q1 2023, and further to 7% in Q2 2023.

As a company known for negotiating, one might assume that Vendr aims to avoid the sticker price. However, our approach is quite the opposite. We firmly believe in fair and transparent pricing and equal access to information – key ingredients which enable faster and smarter transactions between software buyers and sellers.

That is why we have included all the data you need to make informed purchasing decisions in this report. Whether it's our SaaS leaderboard or Community Insights, we have you covered. After all, knowing the price of SaaS is like forecasting the weather. Without the right tools and data, you're simply guessing.

We hope this report helps you navigate the next season ahead. And, just like the weather, big changes can happen quickly. We’ll see you back here next quarter to break it all down again.

SaaS pricing snapshot: ACV hits lowest point in three years

The average Annualized Contract Value (ACV) for all SaaS transactions through Vendr, quarter by quarter.

Why this matters

Analyzing overall ACV across categories allows us to identify broad trends regarding supplier pricing and buyer spend.

Key insights

- Average ACV has dropped by 45% between Q1 and Q2.

- Buyers prioritize efficiency by opting for fewer seats, choosing the most affordable tier, and reducing expenses.

- Products in CRM, Accounting & Finance, and IT Service Management categories experienced the most significant declines in average ACV.

- ACVs are dropping, but it's still the year of the price hike. Prominent suppliers in CRM, project management, and marketing automation have announced plans to raise prices in the near future to combat low contract values. Price hikes may come in response to seat count and tier reductions.

Note: Q1 2023 ACV has been revised to reflect more accurate data reporting.

Average discount rates for all transactions processed through Vendr, quarter by quarter. Vendr tracks discount rate as the delta between the price offered at the beginning and end of the negotiation.

Why this matters

Tracking discounts shows the extent to which suppliers deviate from the listed price. SaaS pricing often exhibits significant variability, and it is valuable to understand how this trend progresses.

Key insights

- Recent surveys from G2 and Morgan Stanley have reported increased willingness to discount, but Vendr’s transaction data tells a different story. Discount rates are clearly decreasing.

- Less discounting paired with lower ACV indicates suppliers are moving toward standardizing list pricing at a level closer to negotiated price.

- Vendr is a pioneer in the price standardization movement, with more than 100 suppliers having joined Vendr Verified and committed to standardized, transparent pricing.

Suppliers with the badge are a part of the invite-only Vendr Verified program. Vendr Verified suppliers have our stamp of approval, and have agreed to a transparent best price and satisfaction guarantee for those buying through Vendr.

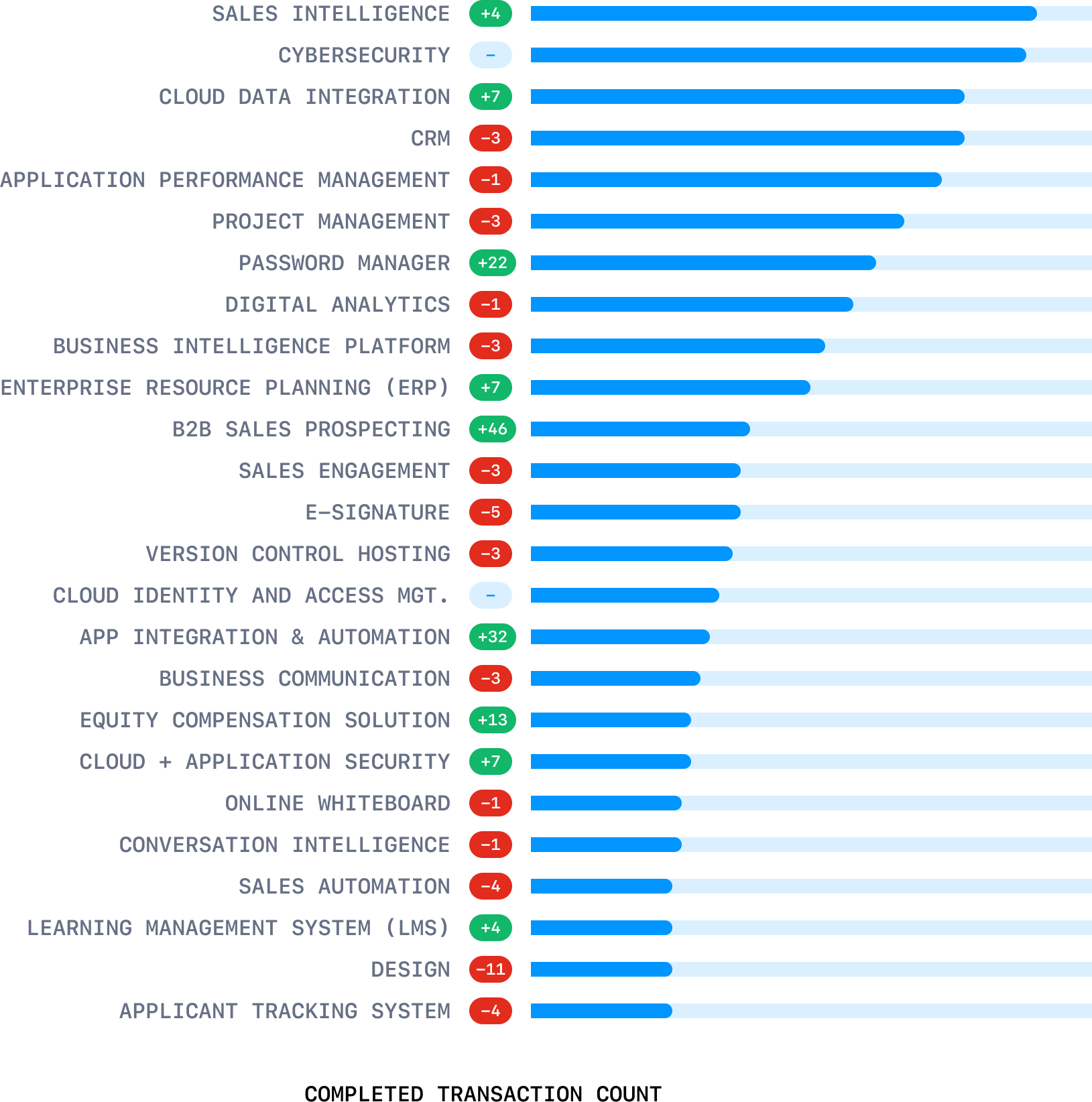

Top-purchased categories

The top categories of Q2 2023 SaaS net new, renewal and month-to-month purchases, broken down by quantity of transactions per category.

Why this matters

This report shows where software buyers spend each quarter, helping CFOs and procurement teams gauge how the industry adjusts and expands tech stacks. These insights also help sellers benchmark performance against peers at the category level. The report also shows quarter-over-quarter change, indicating whether a category rose or fell in popularity from Q1 to Q2.

Key insights

- Password Management, B2B Sales Prospecting, and App Integration & Automation were the categories that climbed the most quarter-over-quarter.

- The top three categories, Sales Intelligence, Cybersecurity, and Cloud Data Integration, reflect companies’ mission-critical needs. Companies continue to prioritize growth through investments in go-to-market products, ensure security, and maintain infrastructure to keep the lights on.

The SaaS Leaderboard: Q2 2023

The top-purchased products through Vendr in Q2 2023, organized by category.

The top three suppliers in each of Vendr’s top categories by transaction volume in Q2 2023.

Why this matters

Even during a challenging quarter, there are software products and companies that continue to provide high-value solutions to help companies. Here, the report highlights the top performers in the most popular categories who consistently bring value to customers, attract new ones, and increase industry market share.

Key insights

- 60% of the category leaders are publicly traded, with an average employee count of approximately 5,000 and a median ACV slightly above $50,000.

- Thirty solutions join this quarter’s leaderboard for the first time.

- SentinelOne, Amplitude, and Workato not only entered the leaderboard for the first time but also emerged as category leaders.

Sales Intelligence

Companies are increasingly investing in Sales Intelligence tools like ZoomInfo and 6sense. These tools provide a data-driven understanding of prospects and customers, enabling more effective sales outreach.

Why this matters

Sales Intelligence tools leverage data and analytics to help companies bridge the growth gap with reduced resources, enabling them to reach the right prospects with the right message at the right time.

Key insights

- Sales Intelligence is the most popular SaaS category, rising five spots since Q1.

- The ACV for Sales Intelligence tools increased by over 20% in Q2.

- With layoffs on the rise, companies are forced to do more with less — that applies to go-to-market. Sales Intelligence products are helping companies continue to prospect at a high velocity and add pipeline with fewer resources.

Top products by ACV

The estimated average ACV and quantity of transactions for leading suppliers in Q2 2023.

Why this matters

The average ACV in this chart tells us where the industry's pricing is moving. Buyers and sellers can assess the position of specific suppliers compared to competitors and alternatives. Additionally, this analysis reveals trends in the popularity of different products relative to ACV.

Key insights

- GTM solutions like Netsuite, Salesforce, ZoomInfo , and LinkedIn dominate the high-transaction and high-ACV quadrant.

- Most transactions fall within the $20K to $80K ACV range.

- Price and stickiness correlate. If company processes are already embedded in a product, buyers are more willing to pay more instead of switching to a different solution.

- Resilient and mission-critical suppliers show consistent growth, while nice-to-have products fall behind in transaction count and ACV compared to Q1.

Top newly purchased products

The top net-new purchased products in Q2 2023.

Why this matters

Right now CFOs are scrutinizing net-new spending more aggressively than ever. By seeing which products receive the stamp of approval, buyers can understand which products are mission-critical.

Key insights

- This list highlights several category leaders, indicating buyers are shifting budgets to the proven products and avoiding taking a chance on newer companies.

- New product purchases emphasize 2023’s mission-critical priorities: growth, sustainability, and security.

These are the mission-critical SaaS categories. Companies still need to grow (go-to-market), keep the lights on (infrastructure), and remain secure (security).

ZoomInfo

LeanData

1Password

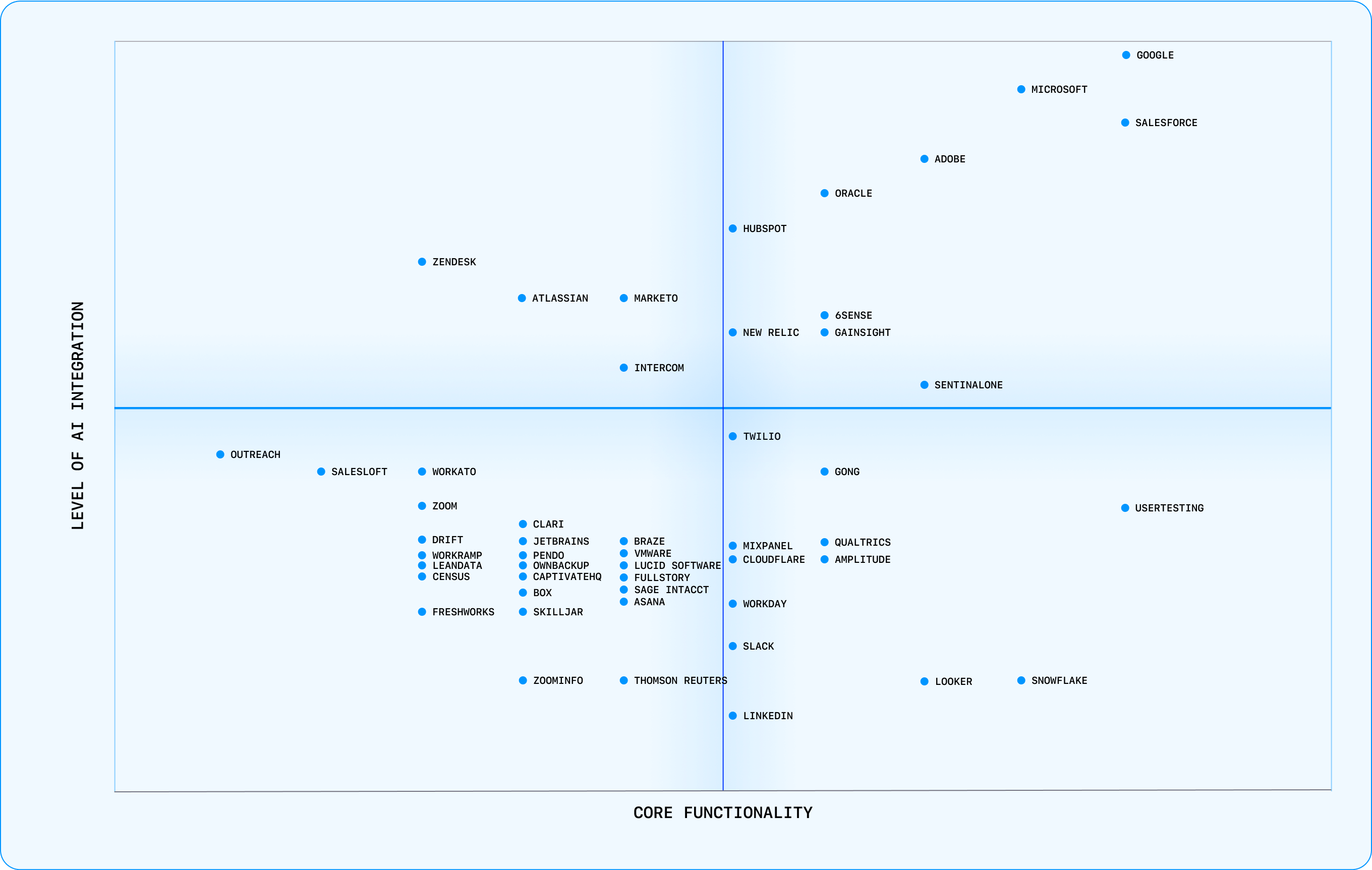

Vendr’s SaaS AI index

Who's dominating the B2B AI race? And, how smaller players join the ranks of the front-runners.

Vendr’s SaaS AI Index evaluates the AI capabilities of top products. The index considers two factors: the extent to which AI is integrated into core functionality, and how effectively an AI implementation enhances value for customers.

Why this matters

AI is a hot topic, but do buyers want AI from SaaS providers? Surprisingly, our data shows that AI integration doesn't strongly influence SaaS purchasing. However, both buyers and sellers should evaluate SaaS AI capabilities to decide if they are useful additions.

Key insights

- Big tech companies like Google, Microsoft, Salesforce, and Adobe lead the way in B2B SaaS with native AI solutions deeply embedded in available products. Salesforce Einstein and Photoshop Generative Fill are impressive AI offerings that deliver immediate impact to customers.

- Companies like Zendesk and Atlassian have developed impressive AI engines, though generally offering less day-to-day value to customers.

- Companies in the lower two quadrants of the index are using AI-integrated solutions to test and release AI features, with varying degrees of adoption, customer satisfaction, and success.

- AI has been embraced more enthusiastically by go-to-market tools, like CRM, sales intelligence, and marketing/sales automation, compared to the broader SaaS ecosystem.

AI enablement

AI-Native

Top tech players like Google, Microsoft, Adobe and Salesforce are creating industry-leading native solutions.

AI-Enabled

Smaller SaaS companies are leveraging the industry-leading tech of top companies to enable products with AI tools.

Community Insights from SaaS buyers

Vendr Community Insights is the world’s largest collection of verified SaaS buying advice. Here are a few of the 1,000+ new Community Insights submitted this quarter.

“Figma will not negotiate terms or pricing. Since they don't offer discounts, our only path for reducing our annual commitment was to reduce the number of users in the account.”

“When working with Glean , it is crucial to establish renewal caps due to significant uplifts ranging from 7-12% and lack of multi-year agreements. Additionally, it is advisable to incorporate pricing tiers within the order form, which Glean agrees to when the user count reaches 200. Fortunately, our agreement included a 5% renewal, but Glean still attempted to enforce it despite our usage growing by 20%. However, thanks to the tiered pricing structure we had in place, we consistently referred to our usage growth as a valid reason for waiving the uplift. After three rounds of negotiations, Glean finally agreed to remove the uplift.”

“We successfully negotiated our renewal pricing with Salesloft , reducing it to approximately $70,000 from the initial quote of around $94,000. Salesloft employed creative strategies with order forms, splitting our 55 users across two lines. Half of the users were billed for 12 months, while the other half were prorated for 6 months but received access for the full 12 months. Salesloft adjusted the start dates for accurate invoicing, ensuring all 55 users had access throughout the entire contract period.”

“Asana, Wrike, and monday.com were in competition to win our business, and Asana was particularly motivated to secure the transaction. Through negotiations, we successfully obtained a 30% discount for the new purchase by emphasizing our budget limitations and highlighting the competitive landscape. Additionally, we were able to secure NET60 payment terms.”

“Chili Piper maintained pricing despite leveraging growth, conducting a case study, securing a multi-year agreement, and facing competition. They emphasized adherence to a "fair billing" policy, ensuring that all customers, regardless of volume or commitment, pay the same amount.”

Q3 predictions

Discounts start disappearing.

Pricing transparency is coming. As more companies streamline sales teams, suppliers are less likely to play games or drag out sales processes. This means you can expect clearer pricing information and fewer discounts driven solely by sales tactics.

The AI surge will benefit incumbents more than startups.

The pace at which established SaaS suppliers and big tech companies have adopted and innovated on AI is remarkable. Given how fast this technology can be rolled into new and existing products, distribution will be the differentiator. The explosion of AI startups will of course produce winners, but in aggregate the biggest winners will be incumbent players who are able to quickly put AI functionality in front of huge userbases.

Stack consolidation will lead suppliers to offer more.

As companies consolidate technology stacks, buyers will purchase fewer new products and avoid ones that lack 80% of the needed features. Suppliers will offer more features, tools, and products in comprehensive suites to become solutions that are consolidated ‘to,’ rather than consolidated ‘from.’ CFOs will focus on getting more value from existing suppliers instead of adding new ones.

The year of the price hike continues.

Get ready for more price hikes as SaaS suppliers manage challenges like declining ACV, reduced seat counts, and need to hit growth targets.

Final thought

Enhancing efficiency goes beyond cost-cutting.

Companies often mistakenly trim the wrong areas, leading to reduced revenue or increased unintended expenses. This era calls for more than cost-cutting — companies need to revolutionize software stacks while preserving efficiency.

This boost is vital for gaining an edge in tough economic times. Organizations can optimize productivity and resource allocation by streamlining SaaS processes and maximizing utilization.

The siloed and secretive nature of the software industry has hindered companies. Identifying shelfware, duplicate spend, and overpriced contracts has become a huge challenge.

However, this chaotic situation is about to change. Vendr’s vision is to eliminate software isolation and empower buyers and sellers to achieve genuine boosts beyond simply reducing costs.

Efficiency and productivity drive success in a competitive landscape. Whether you're a customer or not, join us in envisioning a future where buying SaaS is transparent, efficient, and beneficial for all.